Dude, where's my deposit interest? Also, cash rates, real-time capital gains tax, and when we can and can't make money out of thin air

There's a bit that's been keeping me busy

I've been one poor correspondent

And I've been too, too hard to find

But it doesn't mean you ain't been on my mind

Hello, after so long!

I’ve missed you, and it is my fault. I promised my newsletter would never come out more than weekly, and the last one was three months ago.

In my defence, there have been a few things going on at home that have needed my attention.

But the economic news and conundrums have kept coming, big time, which makes this, and the entire time since COVID the best time in modern history to be an economics columnist. First, forecasts.

The forecasting panel I reconvened at the beginning of the year produced predictions that are – so far – holding up well. (My cartoonist Wes Mountain was still getting the hang of our new crop of decision makers.)

Here is its key forecast:

Ten hikes in a row and this month’s pause has taken the cash rate to 3.6%, which is close to the forecast peak.

The futures market believes rates have peaked. It expects a decline form here on. And much as I hate to say it, the futures market has been more accurate than economic forecasters for a year or more now.

So why did the RBA stop hiking? Here’s my account:

I discussed this with Centre for Independent Studies Chief Economist Peter Tulip and Gillian Bowen on an episode of her podcast Making Money Easy that dropped on Easter Monday. (We recorded it on Good Friday) . Although I haven’t listened back, I heard it as we did it, and Peter Tulip is always worth listening to.

And I discussed the end of cheap money with the excellent Nicki Hutley and Geraldine Doogue on Saturday Extra in March. I was of the view that it won’t make much difference, for reasons Ian McAuley summarises:

Businesses and governments failed to take up the opportunity to invest when rates were low – when, in real terms, money was free. Businesses (conditioned by a hundred years of high returns) applied high hurdle rates to new investments (generally returning profits to shareholders rather than re-investing), and governments similarly failed to borrow for necessary infrastructure. Households, however, did respond, and their borrowing for “investment properties” resulted in extreme house-price inflation.

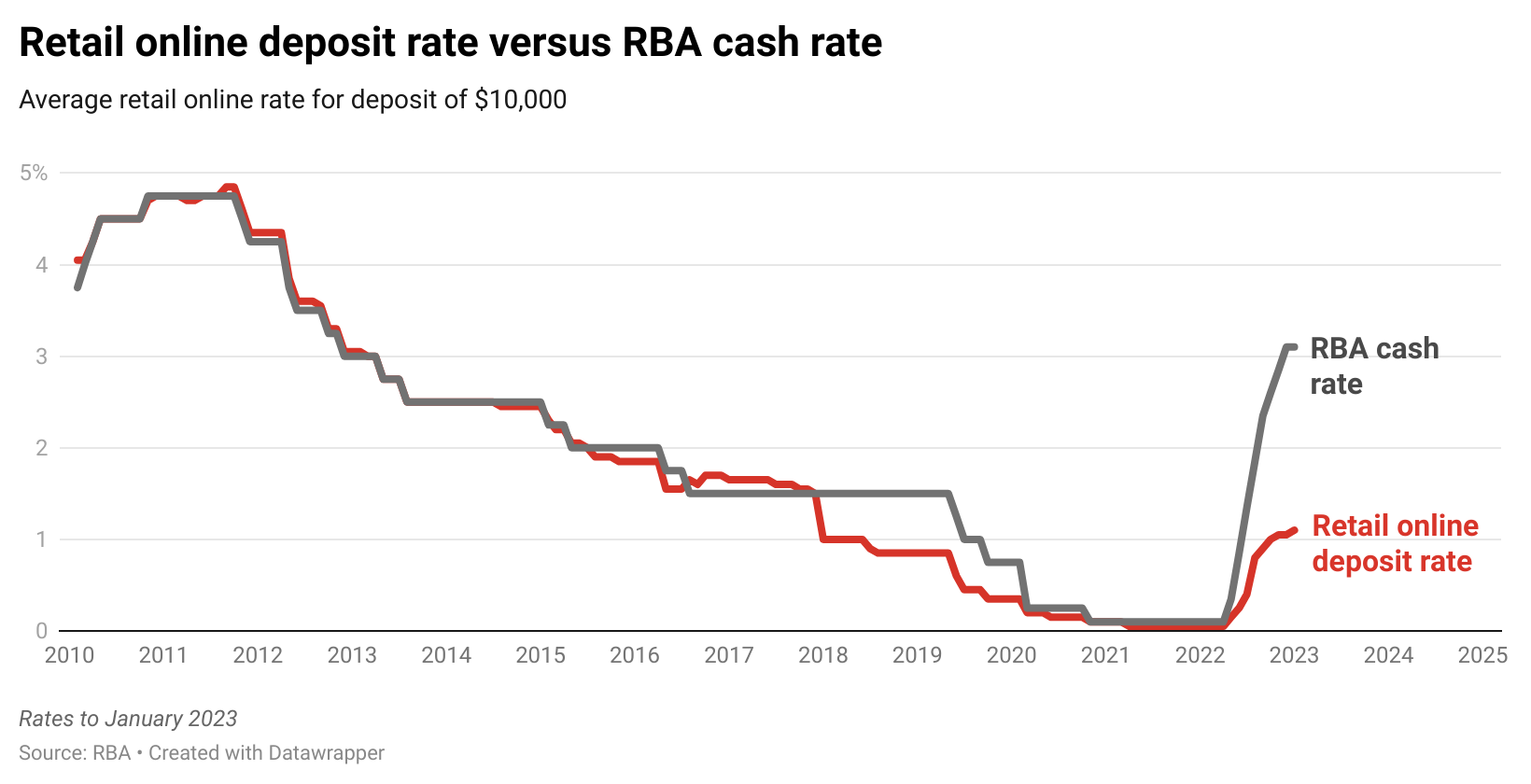

Dude, where’s my deposit interest?

In February, I examined why Australia’s biggest banks had stopped had paying proper interest on deposit accounts (things have improved a bit since).

Each of the big four used to pay depositors the cash rate, then each stopped:

Why did they stop? (And why did they stop in a synchronised manner?)

In very recent years, the banks have had less reason to offer high rates. During the first 15 months of COVID, the Reserve Bank made available A$188 billion of funding to banks at the extraordinarily low rates of 0.25% and 0.1%.

This meant banks had less need to attract deposits, and in any event, they were overwhelmed with deposits. Elevated savings rates during COVID pushed an extra $300 billion through their doors, as worried and locked-down households sought out safe places to stash cash.

Each of these things is ending, so it’s increasingly worthwhile to shop around… BUT don’t believe Anna Bligh of the Australian Banking Association on this topic. Here’s what she said in February:

“This time last year, the four major banks, nobody, no bank was offering more than 0.3% on their savings account,” she told the Australian Financial Review this month. “Right now, they’re all offering at least 4% or more. So that’s a massive increase.”

As I note, the rates Bligh quotes are unusual ones – anything but standard.

The Commonwealth Bank is indeed paying 4% on its so-called NetBank Saver account, but the 4% is an introductory rate for new customers only – before slipping back to 1.6% after five months.

And some of the high-looking rates have special conditions. The Commonwealth’s GoalSaver account also offers 4%, but only if you put in more money in each month. If you can’t, or if you make a withdrawal, the rate plummets to 0.25%.

It looks as if the big banks are doing to deposit rates what the big phone companies did to the price of calls, and the electricity companies did to the price of power, and the private health organisations did to the price of insurance – making the price so hard to calculate we can’t can’t work out whether to switch. They are about to face an ACCC inquiry.

Speaking of deposits…

Deposit interest is taxed more or less as it accrues, each year.

But (originally for reasons of convivence rather than tax theory) capital gains have been taxed only when they are “realised” (the asset is sold)

The 2010 Henry Tax Review saw this special treatment as a problem.

The Henry Review said collecting tax only on “realisation” (when assets were sold) rather than “accrual” (as they grew in value) encouraged investors to hold on to shares and property to delay paying tax – a response it called “lock-in”.

All the better for the investors if, when they eventually sold, they had retired and were on a much lower tax rate, meaning they would scarcely pay any tax on decades worth of gains.

During financial crises when prices fell, the rules encouraged investors to do the reverse – to sell quickly to realise tax losses, destabilising markets.

Henry would have preferred tax to be collected as the gains accrued, but said back then that wasn’t practical.

Taxing capital gains each year as they accrue is practical now, and the good news (in my view) is that Chalmers plans to do it, at first in a small why, for the extra tax on large super accounts due to come in in 2025.

As it happens, one of the reasons is that it actually more straightforward to tax super funds that way.

Rather than taxing capital gains only when assets are sold (as will still happen for the bulk of what’s in super accounts), the surcharge will be calculated by applying a 15% tax rate to the increase in the value of the relevant part of each fund. Super funds are already valued quarterly.

Chalmers isn’t talking about doing it more broadly. But what he is doing shows it would be fairly easy.

Here’s why it has become easy:

Firms such as CoreLogic revalue property daily, and not just in the general sense. If you want to know what has happened to the value of a three-bedroom home with two bathrooms, on a particular size block of land, in a particular street, CoreLogic can tell you.

And real-time values are being used for all sorts of purposes. Pensioners owning rental properties get their value updated annually for the pension assets test. Services Australia doesn’t wait until they are sold to declare they are worth more.

It is the same with council rates. Property values are updated annually, rather than down the track when they change hands. There’s no longer a practical impediment to doing this, and there’s never been a practical impediment to valuing shares. They are valued daily on the stock exchange.

I reckon the time is coming. Taxing capital gains in real-time on a mark-to-market basis (as Denmark is about to do) would make it possible to apply capital gains tax to high-end “family homes”, without causing lock-in.

We will need more tax

Ken Henry reckons so. His truly excellent address to the Tax Institute in February is here, and the slides here.

For The Conversation and the Economic Society of Australia I surveyed 59 leading economists to select what should be done from a limited menu of options informed by the 2022-23 Tax Expenditures Statement and their preferences were fairly clear.

(I should add that I asked them to reply as if political constraints were not a problem.)

We’ve printed all of the responses, expert by expert. They are worth reading.

Money from nothing

But hang on, do we even need to raise more tax? Can’t we just spend more, like we did during the first two years of COVID?

The answer is, “sometimes”, or as I put it in a piece intended to outline modern monetary theory:

The deeply unsatisfying answer is that, from an economic perspective, it depends on who else is spending what at the time.

In the first year of the pandemic, Australians were given a glimpse of a truth so unnerving that economists and politicians normally keep to themselves.

It’s that, for a country like Australia, there is “no simple budget constraint” – meaning no hard limit on what we can spend.

“No simple budget constraint” is the phrase used by Financial Times’ chief economics commentator Martin Wolf, but he doesn’t want it said loudly.

The problem is, he says, “it will prove impossible to manage an economy sensibly once politicians believe there is no budget constraint”.

A quick look at history shows he is correct about there being no simple budget constraint, despite all the talk about the need to pay for spending.

As you can see below, Australia’s Commonwealth government has been in deficit (spent more than it earned) in all but 17 of the past 50 years. The US government has been in deficit for all but four of the past 50.

Commonwealth government surpluses and deficits since 1901

There is no hard limit on how the Commonwealth can spend over and above what it earns, just as there’s no hard limit on how much you and I can spend. But whereas you or I have to eventually pay back what we have borrowed, governments face no such constraint.

Because the Commonwealth lives forever, it can keep borrowing forever, even borrowing to pay interest on borrowing. And unlike private corporations, it can borrow from itself – borrowing money it has itself created.

One way to think about it (the way so-called modern monetary theorists think about it) is that none of the money the government spends comes from tax.

The government creates money every time it gets the Reserve Bank to credit the account of a private bank (perhaps in order to pay a pension), and destroys money every time someone pays tax and the Reserve Bank debits the account.

If it creates more money than it destroys, it’s called a budget deficit. If it destroys more than it creates, it’s called a budget surplus.

Can creating money out of thin air go on forever?

No, but where it should stop is a matter for judgement.

If it spends too much money on things for which there is plenty of demand and a limited supply, it’ll push up prices, creating inflation.

Where to stop will depend on how much others are spending.

If there’s little demand (say for builders, as there was during the global financial crisis) the government can safely spend without much pushing up prices (as it did on builders during the global financial crisis).

If it wants to spend really big (say on building submarines), it might have to restrain the spending of others, which it can do by raising taxes.

But it’s not a mechanical relationship. The main function of tax is not to pay for government spending, but to keep other spenders out of the way.

That’s it for now. I’ll be a better correspondent next time.